July 2025 - Market Recap

Summary

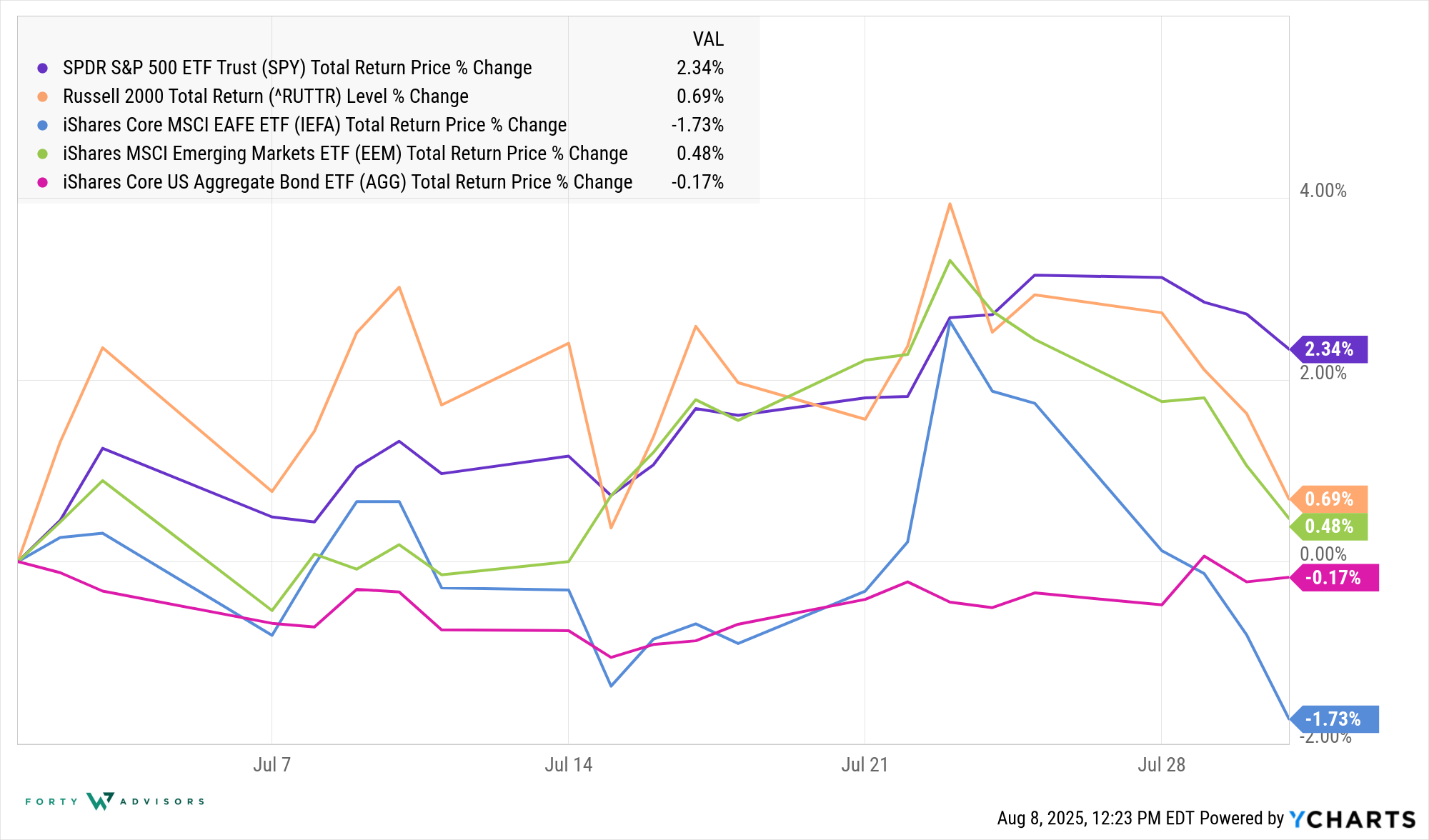

In July, US equity markets had a positive month overall, with large-cap stocks (S&P 500 - SPY) slightly outperforming small-caps (Russell 2000). On the international front developed markets (IEFA) were negative after a stellar first half of the year. Emerging markets (EEM) proved relatively resilient compared to Europe and Japan, even as global trade and growth concerns hung over markets.

Core aggregate bonds (as shown by AGG) posted a modest loss of -0.17%, pressured by rising yields for most of the month before a late rally. High-yield bonds outperformed, benefiting from a supportive risk environment and less rate sensitivity.

Economy

The US economy accelerated in July on strong services activity, even as job growth decelerated and manufacturing faced pressure from tariffs and costs. Globally, economic momentum was uneven—with EU growth flat, China’s manufacturing weakening, and Japan holding steady. The global economic environment was shaped by shifting monetary policies and a volley of new tariffs, contributing to softer business sentiment and rising inflation risks.

The Federal Reserve left its policy rate unchanged at 4.25%-4.50%. Notably, two Fed governors dissented in favor of a rate cut, citing moderating growth.

We continue to keep an eye on inflation as tariff effects should start to show their impact as well as the labor market. Any future rate cuts will be dependent on these two data points:

US Equities

US equity markets had a positive month overall in July 2025, with large-cap stocks slightly outperforming small-caps. However, heightened volatility at month-end reflected mounting economic and policy uncertainties.

- Early Gains and Record Highs:

Through most of July, both S&P 500 and Nasdaq Composite indices reached new all-time highs, buoyed by strong earnings from several mega-cap technology firms that represent a large share of the S&P 500 index. - Late-Month Volatility:

The market turned lower in the final days, primarily due to:- A significantly weaker-than-expected July jobs report (nonfarm payrolls rose by only 73,000 vs. 104,000 expected).

- Two months of large downward revisions to job growth, indicating softening labor market conditions.

- President Trump’s announcement of new tariffs (ranging from 10% to 41% on imports from several countries).

- Sector Performance:

Leadership came from healthcare and consumer staples. In contrast, consumer discretionary was the biggest laggard, influenced by high-profile post-earnings declines in names like Amazon.com and Apple Inc..

Business expenditures on technology, specifically artificial intelligence continue to drive US equity market performance despite subdued economic activity in the labor markets and manufacturing.

International Equities

Developed International - Europe & Japan

The MSCI EAFE Index (tracked by iShares MSCI EAFE ETF (EFA)) represents developed markets in Europe and Japan.

- In July 2025, the EFA returned -1.93%, signaling a negative month for developed markets outside the U.S.

Trends and Drivers:

- European equity performance was mixed and at times choppy, influenced by trade headlines, earnings fluctuations, and macro data.

- Sentiment improved when an initial trade deal between the US and both Japan and the EU was announced, lowering anticipated tariffs.

- Tech and retail shares struggled at times, while property and banks often outperformed on strong earnings or optimism about rate cuts.

- Volatility indices such as the Euro Stoxx 50 VIX remained mostly below 20, indicating market conditions were not excessively turbulent.

- Japan's equity market had periods of strength, especially after optimism about the US-Japan trade deal and the Bank of Japan’s steady policy stance, though elsewhere in Asia sentiment was more cautious.

Emerging Markets

- In July 2025, the EEM returned +0.48%, indicating a modestly positive result and general outperformance against developed markets ex-U.S.

Trends and Drivers:

- Emerging markets proved relatively resilient compared to Europe and Japan, even as global trade and growth concerns hung over markets.

- Markets responded positively to signs of stabilization in Chinese services activity (China’s services PMI beat expectations at 52.6 vs. consensus 50.4).

- Some emerging markets benefited from shifting global supply chains and an improved commodities outlook.

- However, risks from U.S. tariffs (particularly affecting India) and cautious global fund flows kept returns muted overall.

Fixed Income

For July 2025, core aggregate bonds (as shown by AGG) posted a modest loss of -0.17%, pressured by rising yields for most of the month before a late rally. High-yield bonds outperformed, benefiting from a supportive risk environment and less rate sensitivity. The key drivers were volatile Treasury yields, shifting Fed expectations, strong economic data early in the month, weaker jobs data late, and the onset of new tariffs.

Key Market Drivers & Trends in July 2025

1. Treasury Yields Movement:

- The month was volatile for rates. Early in July, yields drifted higher as Q2 economic growth data beat expectations and July job gains outpaced consensus, leading to declines in broad bond prices—including the AGG.

- At the very end of the month, yields fell sharply after a weaker-than-expected July jobs report (with a surprise downside in nonfarm payrolls) and new tariff announcements from the White House. On August 1, the 10-year Treasury yield dropped by -15.3 basis points to 4.22%, signaling a late bounce in government bond prices.

2. Credit Market Conditions:

- Investment grade bonds (the bulk of AGG) saw pressure from early-month yield increases.

- High-yield bonds, less sensitive to interest rates and more to economic and credit conditions, were comparatively resilient. The “risk-on” tone for most of July (buoyed by solid corporate earnings and steady GDP growth) supported high yield prices.

3. The Fed and Rate Expectations:

- Rate cut expectations sharply increased late in July as the jobs data weakened. This led to a rally in rates-sensitive sectors (like Treasuries) at the margin, but not enough to turn the monthly return for aggregate bonds positive.

4. Tariffs and Volatility:

- The announcement of new and increased tariffs late in the month contributed to market volatility and a “flight to quality” at month-end, but its full impact will likely be felt more in August.