Investing: Long-Term Planning Using Capital Market Assumptions

Introduction to Capital Market Assumptions

At Forty W, we believe financial planning is a multi-faceted process which balances a wide variety of inputs and variables to inform financial decision making. Among the many steps that must be taken in building a financial plan is designing an investment portfolio that appropriately aligns risk and return while supporting cash flow needs throughout the duration of the plan. The expected risk and return of the investment portfolio are key inputs for financial modeling and wealth forecasting and are primarily determined by the portfolio’s strategic asset allocation. The importance of the strategic asset allocation is well documented in academic literature and the process by which we arrive at an appropriate allocation for each client needs to be rigorous, practical, and objective.

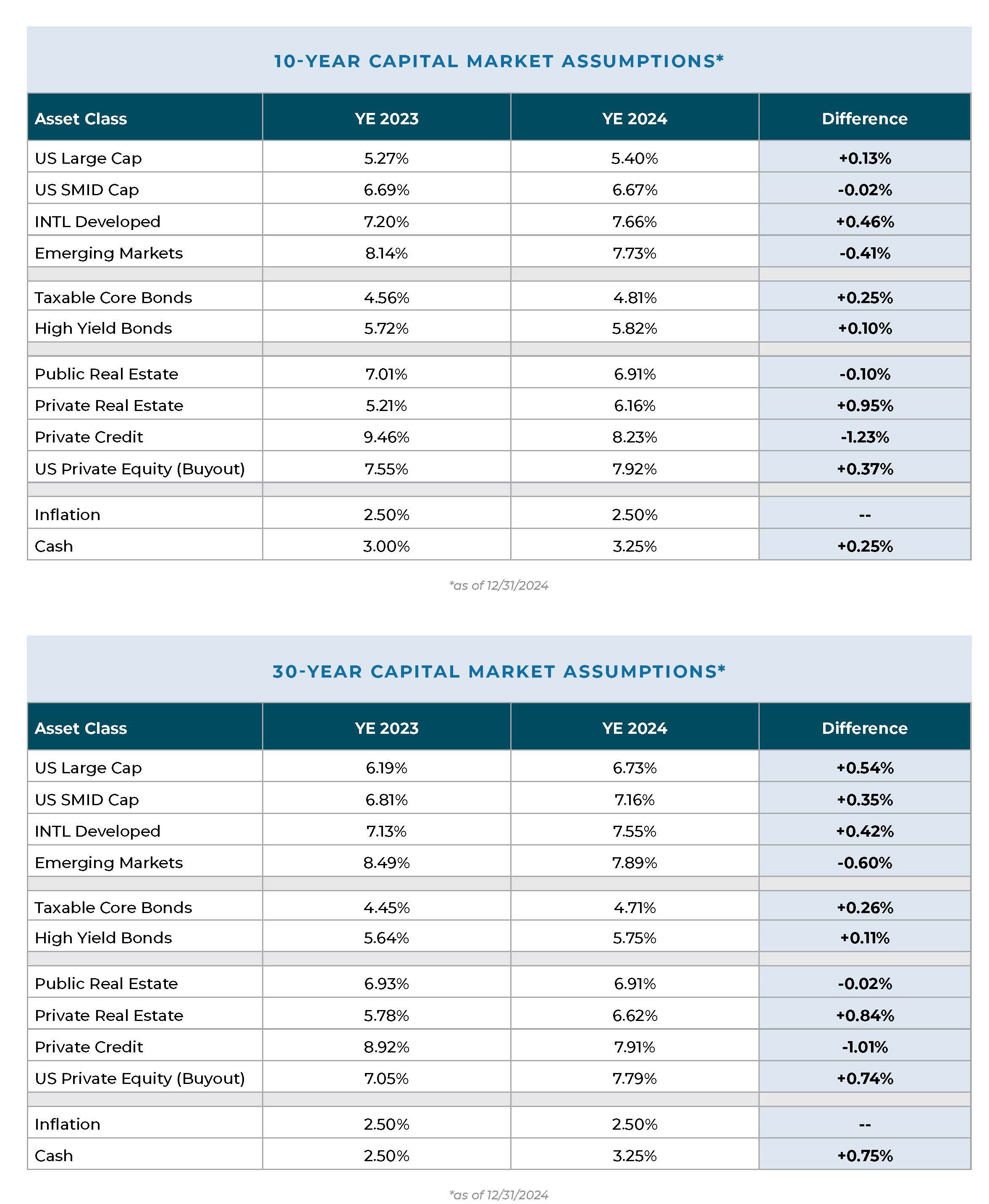

Each year, our Investment Team undertakes a comprehensive review of our capital market assumptions (CMAs) across asset classes. CMAs serve as the foundation of our portfolio construction process because they represent our forecasts for how different asset classes (such as stocks, bonds, real estate, and alternative investments) may perform going forward. As part of this process, we conduct a deep review of projected returns, risk, and correlation data from multiple third-party sources, along with our own internal estimates to arrive at a blended, consensus view for each asset class over 10-year and 30-year time horizons. The data is then used to approximate the efficient frontier and evaluate tradeoffs between allocating to different types of investments.

2025 - Markets at an Impasse

Even before the balance of global trade was thrown into flux in early April, markets were sitting in a precarious position. A multi-year equity rally pushed valuations to historically high levels and the prolonged dominance of mega cap tech stocks culminated in a market that was more concentrated than at any other point in recent history. Coming into 2025, this dynamic was largely justified by record profit margins, strong economic momentum, and rising labor productivity. But with assets “priced to perfection”, markets were vulnerable to an exogenous shock.

That shock arrived sooner than many anticipated when the Trump Administration proposed wide ranging tariffs on April 2nd on trading partners around the world. Market volatility spiked to levels typically reserved for a financial crisis. The benefit of a 10- and 30-year perspective for capital market assumptions is that it affords us the luxury of looking beyond short-term market volatility to focus on the longer-term data that informs our strategic views.

The market volatility that we experienced in early 2025 was in many ways emblematic of one of our key takeaways from this year’s process, which is that the range of potential outcomes for markets is expanding. The table below shows the range of return forecasts provided to us by our third-party partners across several key asset classes.

Relative to a year ago, the dispersion of expectations for most asset classes materially expanded with the exception of International Developed Equities and Core Taxable Bonds, which saw modest reductions. In our view, this is reflective of the increased uncertainty that tends to permeate through markets during the later stages of the economic cycle.

2025 CMA Results

Our updated capital market assumptions reveal a relatively flat stock-bond frontier and suggest a setup more reminiscent of what might be expected during the later stages of an economic cycle (muted equity returns and elevated rates). Below are a few key takeaways from the data:

- The efficient frontier remains relatively flat and relative value opportunities are apparent within and across asset classes. As such, investors should expect to be compensated less for adding incremental equity risk to a portfolio.

- With the exception of Q1 2025, US large cap stocks have enjoyed an extended run of outperformance and valuation multiples reflect a highly optimistic view of the future. Value- conscious investors should look to international markets for pockets of relative opportunity, especially given the backdrop of potential long- term adjustments to the balance of global trade. Read more here: Equity Outlook: US vs. International

- Stocks enjoyed a ~10% annualized return advantage over bonds during the past 10 years. We expect the next 10 years to look very different.

- Within fixed income, investors should be thoughtful about maximizing after-tax returns. Muni/Treasury ratios are near all-time lows, which suggests a higher allocation to taxable bonds might be appropriate for many investors, particularly those who are looking to invest new cash into fixed income.

- Cash assumptions continued to move higher as a result of elevated interest rates. For the first time in many years, there may be opportunities for cash to generate positive real returns. However, investors should be careful not to over-allocate to cash as its short duration nature hinders its ability to produce long-term compound growth.

- Private markets represent an avenue for investors to expand the opportunity set and gain exposure to segments of the market that may have been historically inaccessible. Investors with the capacity to take on illiquidity and understand the unique risks associated with private investments may find that private strategies offer a more attractive trade-off between risk and reward while also offering better diversification.

Disclosures:

This information should not be construed as a recommendation, offer to sell, or solicitation of an offer to buy a particular security or investment strategy. The commentary provided is for informational purposes only and should not be relied upon for accounting, legal, or tax advice. While the information is considered to be reliable, Forty W Advisors cannot guarantee its accuracy, completeness, or suitability for any purpose, and makes no warranties with regard to the results to be obtained from its use. If the reader chooses to rely on the information, it is at reader’s own risk.

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, there can be no assurance that the future performance of any specific investment or investment strategy, including the investments and/or investment strategies recommended and/or undertaken by Forty W Advisors, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Forty W Advisors is engaged, or continues to be engaged, to provide investment advisory services. you should not assume that any discussion or information contained in this presentation serves as the receipt of, or as a substitute for, personalized investment advice from Forty W Advisors. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request or at www.fortywadvisors.com/disclosures. The scope of the services to be provided depends upon the needs and requests of the client and the terms of the engagement.

Please Note: Capital Market Projections/Forward Looking Statements/Material Limitations. Projections and forward-looking statements (the “Projections”) are not historical facts. The Projections in this presentation are subject to inherent limitations and qualifications and are based on a number of assumptions. The Projections involve risks and uncertainties, including statements as to: (i) general volatility of the securities markets; and, (ii) changes in governmental regulations, tax rates, interest rates and similar matters. The Projections are based on beliefs, assumptions, and expectations, taking into account currently available information, including historical data. These beliefs, assumptions, and expectations can change as a result of many possible events or factors, not all of which are known to us or are within our control. If a change occurs, actual performance could be materially different from the Projections. The Projections should not be construed or relied upon as an absolute probability that a different result (positive or negative) cannot or will not occur. To the contrary, different results could occur at any specific point in time or over any specific time period. The purpose of the projections is to provide a guideline to help determine which scenario best meets the client’s current and/or current anticipated financial situation and investment objectives, with the understanding that either is subject to change, in which event the client should immediately notify Forty W Advisors so that the above analysis can be repeated.

Please Further Note. Different types of investments and/or investment strategies involve varying degrees of risk and volatility, and at any specific point in time, or over any specific time-period, any investment or investment strategy can and will suffer losses, at times substantial losses. Positive performance should be considered secondary. The purpose of this presentation is to help you to determine if you are willing and able to accept the volatility and risk of loss corresponding to a specific portfolio strategy. Forty W Advisors recommends and/or manages different types of portfolio strategies. If you cannot tolerate the volatility and potential loss associated with a specific portfolio strategy, Forty W Advisors will introduce a different strategy to you for your consideration. Forty W's goal is to help you identify a strategy that best matches your investment objective and risk tolerance.

Note that these asset class assumptions are passive, and do not consider the impact of active management. Given the complex risk-reward trade- offs involved, we advise clients to rely on their own judgment as well as quantitative optimization approaches in setting strategic allocations to all the asset classes and strategies. Because of the inherent limitations of all models, potential investors should not rely exclusively on the model when making an investment decision. The model cannot account for the impact that economic, market, and other factors may have on the implementation and ongoing management of an actual investment portfolio. Unlike actual portfolio outcomes, the model outcomes do not reflect actual trading, liquidity constraints, fees, expenses, taxes and other factors that could impact future returns. Asset allocation/diversification does not guarantee investment returns and does not eliminate the risk of loss.

©2025 Wealthspire Advisors.