2025 Mid-Year Investment Report

This content is as of 06/30/2025. Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance. Investing involves risk, including loss of principal. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Indices referenced: US Large Cap - S&P 500 and S&P 500 equal weight, US Small Cap - Russell 2000, Developed Int’l – MSCI EAFE, Emerging Markets – MSCI Emerging Markets, Core Bonds – Bloomberg US Aggregate, High-Yield – Bloomberg US Corporate High-Yield

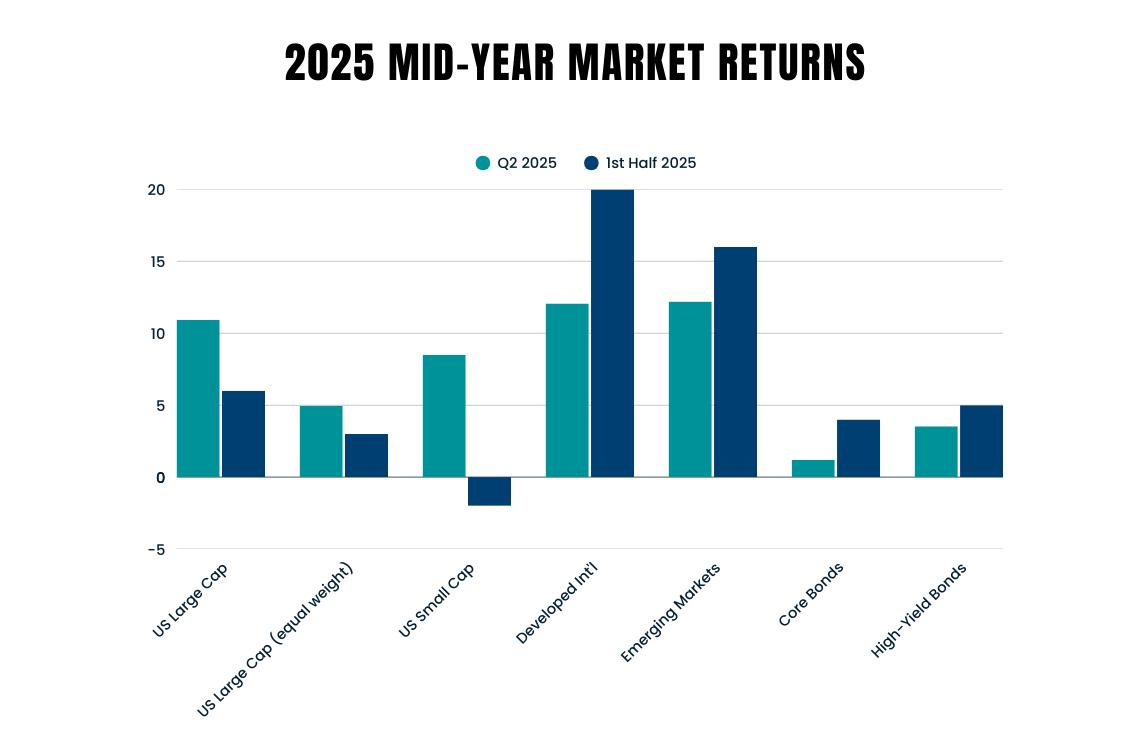

US Equities – Positive First Half for Large Cap Stocks Despite Lots of Turbulence

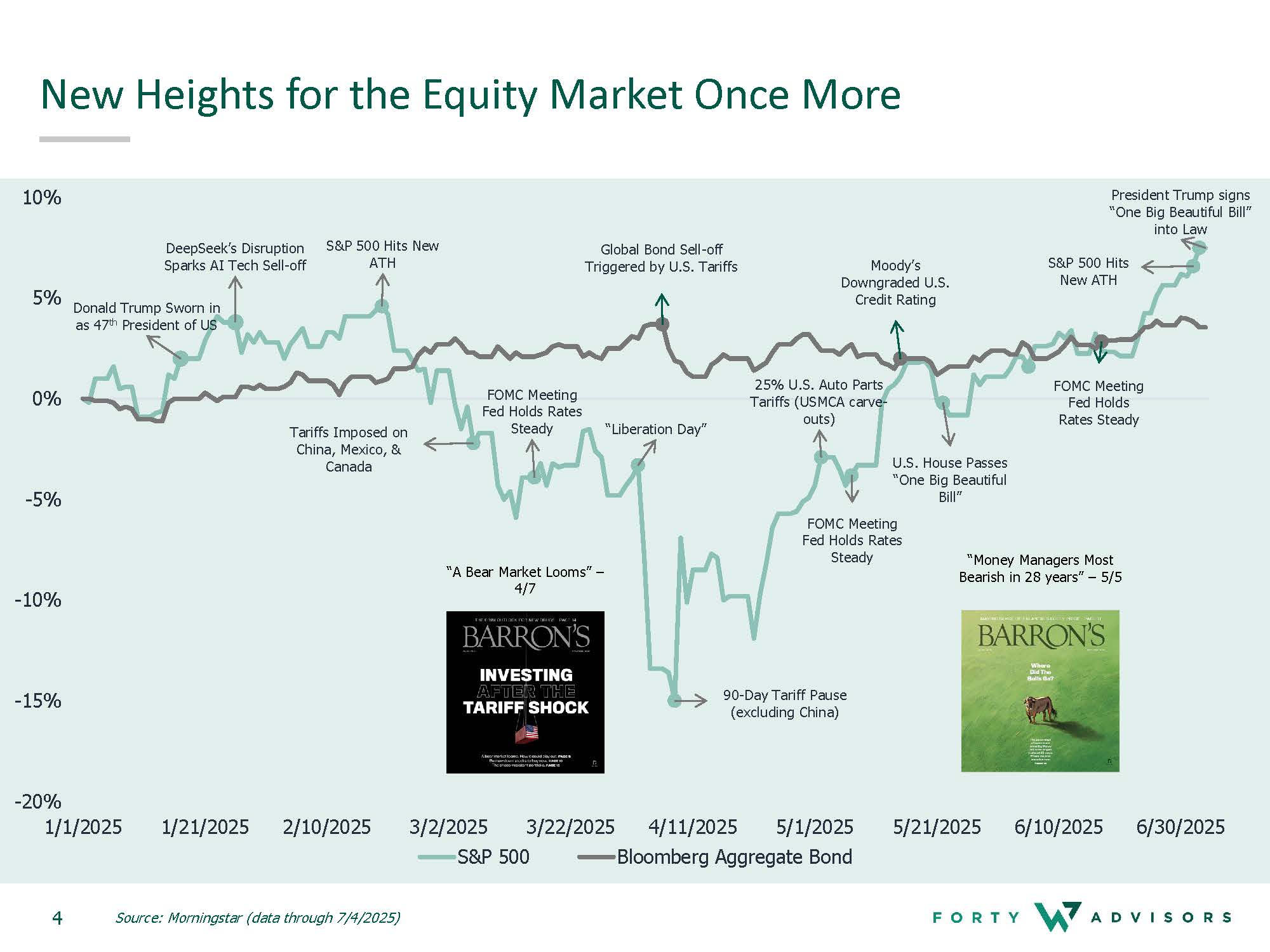

The first half of 2025 delivered a tale of two quarters for US equity markets, characterized by significant volatility that ultimately resolved in modest positive returns across major equity indices. While the S&P 500 gained 6.20% and the NASDAQ advanced 5.85%, these headline numbers masked considerable intra- period turbulence driven by geopolitical tensions, persistent inflation concerns, and evolving Federal Reserve policy expectations. The period highlighted the fact that equity markets, particularly when trading at elevated valuations, can be very sensitive to uncertainty.

Looking forward there is reason to remain optimistic about continued momentum, much of the uncertainty is behind us, the tax bill has passed, there is more clarity on the administration’s regulatory priorities and the economy (at large) and corporate earnings continue to grow. However, we are not entirely out of the woods. The most immediate threats will be any escalation to tariff rates leading up to the most recent deadline of August 1st as well as signs that the already imposed universal tariffs are starting to impact inflation and/or corporate earnings.

US Small Caps – Negative First Half despite Q2 rally

Small cap stocks faced a challenging start to 2025 but showed signs of recovery in the 2nd quarter. Small-cap stocks suffered from the same issues as the broader US market but sold off to a greater extent. Sentiment did improve in Q2 as inflation slowed, the Fed signaled potential rate cuts, and valuations reached historically attractive levels. While small caps lagged large caps overall, a shift toward growth names, improved macro-economic clarity and improved regulatory environment suggest potential tailwinds heading into the second half of the year.

From a longer-term perspective, these domestically focused companies stand to benefit from onshoring trends, infrastructure spending, and proposed tax reforms.

International Stocks – Dominant Start to 2025

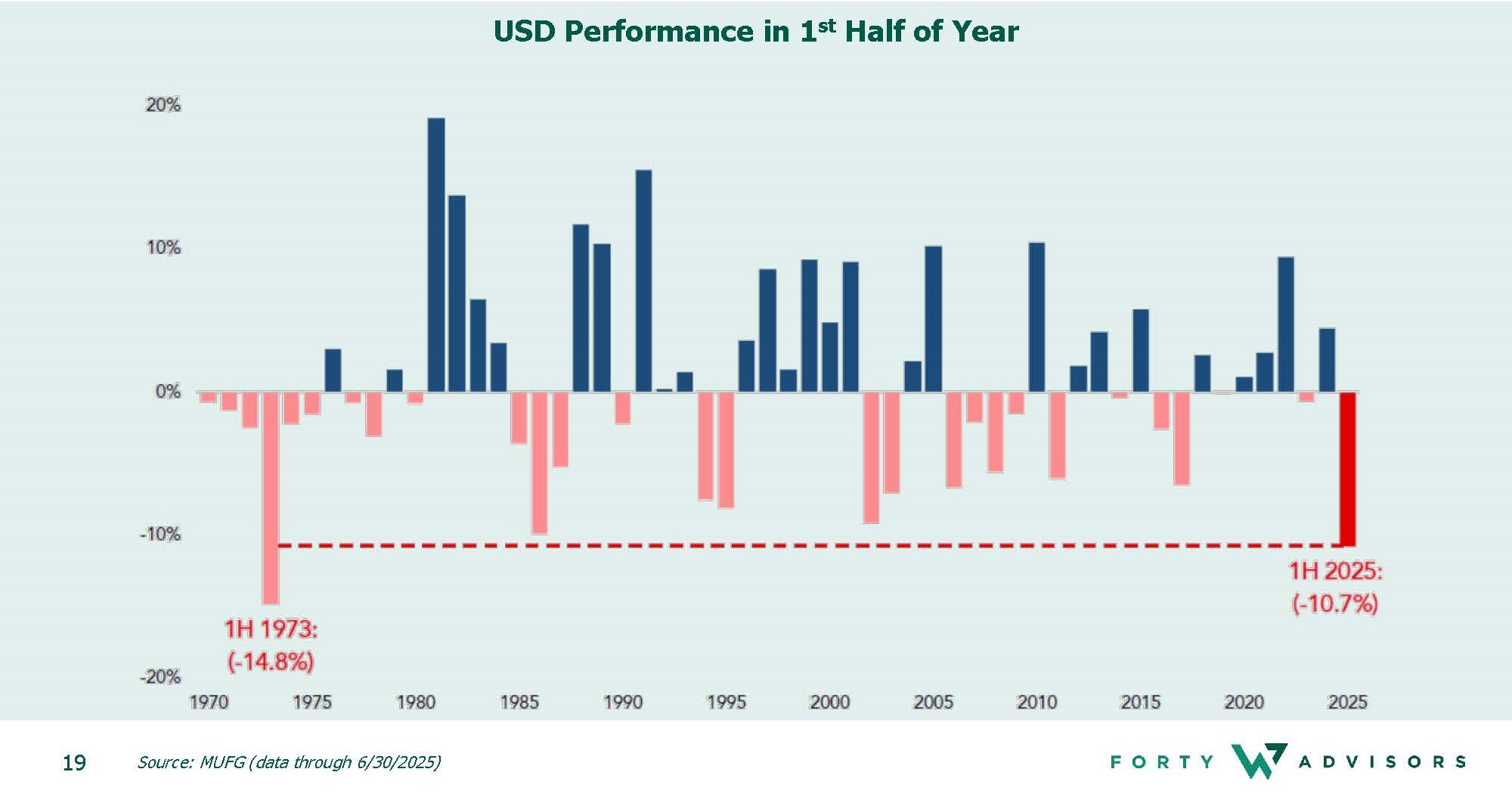

A notable occurrence so far this year has been the outperformance of international stocks. The developed markets index, primarily Europe and Japan surged +20% while the emerging markets index was up over 15%. The primary driver this quarter for international stocks was the decline in the US Dollar. The dollar suffered its worst first half of a year since 1973 (-10.7%), which was highly stimulative for international assets.

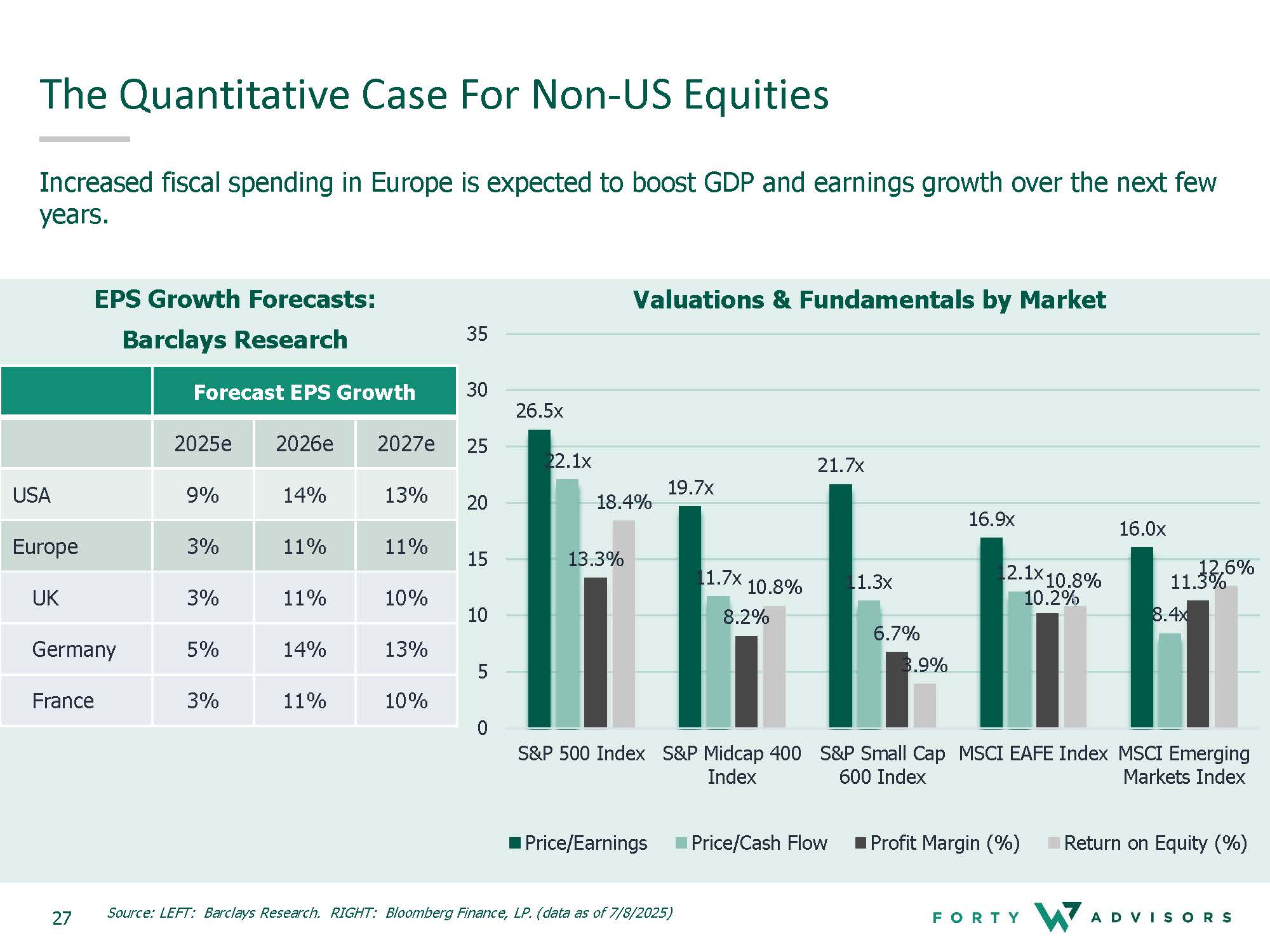

We don’t expect the dollar to continue to fall but we do see additional support for international equities moving forward (which is also noted in our long-term capital market assumptions):

- Germany is leading a fiscal awakening in Europe: After years of austerity Germany now plans to spend about 25% of GDP on defense and infrastructure projects over the coming decade.

- Monetary policy easing: US protectionist policies are deflationary for our trading partners, with inflation not of concern foreign central banks have more flexibility to loosen policy.

- European governments are looking inward: Trump’s “America First” has served as a catalyst for a more unified economic agenda across Europe. The European Commission has announced plans to reduce regulation and make it easier for European business to access capital, especially those that operate in “strategic” sectors.

- Valuations remain attractive relative to US equities and the forecast for earnings growth look strong.

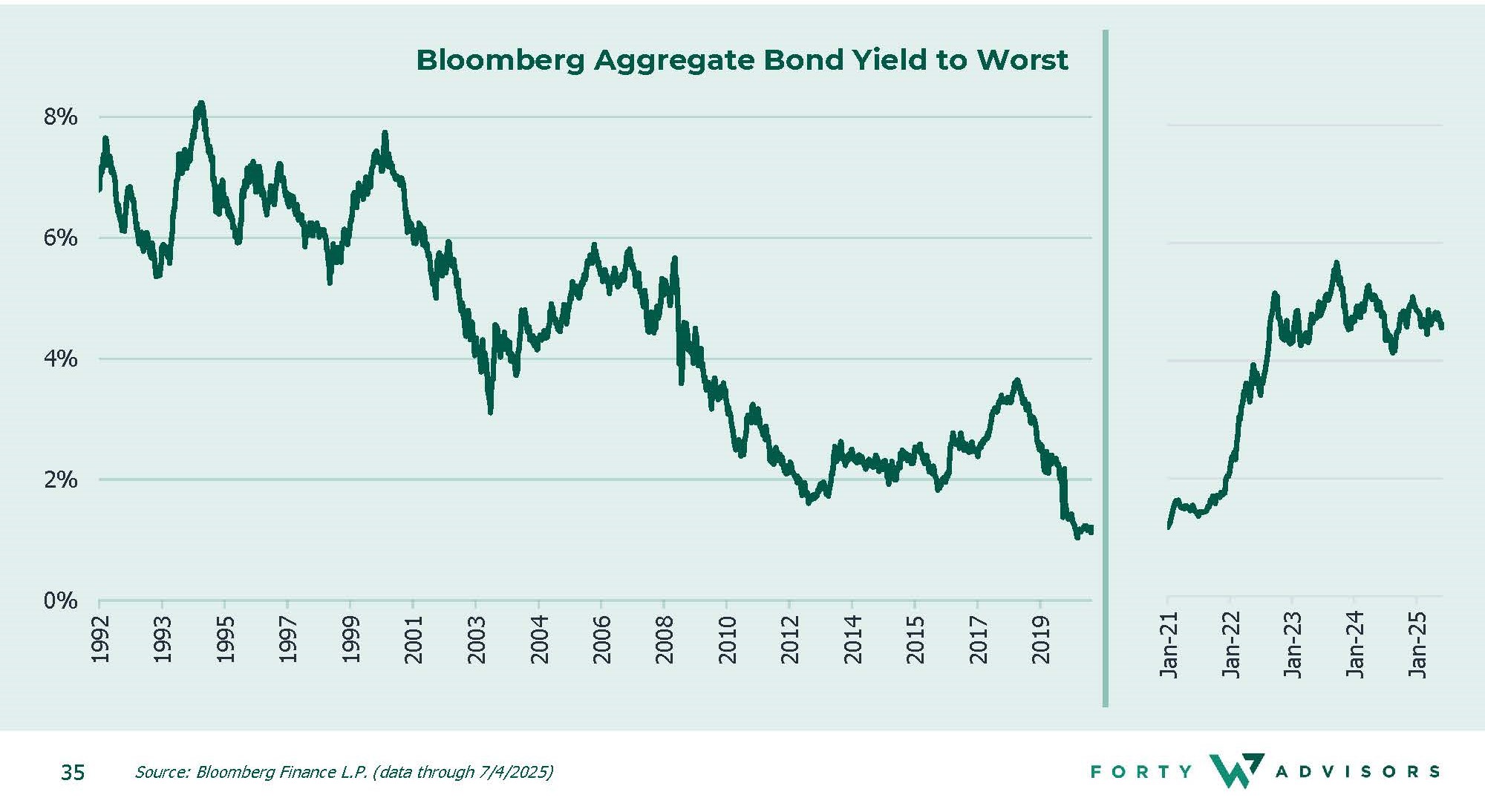

Fixed Income – Bonds provided solid returns and yields remain attractive

The bond market delivered solid, positive returns in the first half of 2025, with most high-quality fixed income sectors up by low- to mid-single digits. Bonds provided stability amid equity market volatility, and yields remained attractive compared to recent years. The core bond index was up 4%. As risk appetite improved in the 2nd quarter high-yield bonds rebounded from a lackluster start to the year and finished +5%.

Starting yields, which is the income you are paid to hold bonds, are one of the things that make taxable bonds attractive in the current environment. Core bond yields have held steady around 4.5% for the last couple of years, something investors have not experienced since the beginning of the decade prior to the financial crisis. Holding bonds with 4.5%+ yields with inflation at 2.5% provide a positive real return with the possibility of further returns via price appreciation IF interest rates were to fall.

Looking Ahead

Looking ahead, the market's trajectory will likely depend on the successful navigation of multiple complex challenges, including the re-emergence of tariff headlines, inflation concerns, the Federal Reserve’s interest rate policy and geopolitical stability. We believe investors should remain vigilant to both opportunities and risks while maintaining a focus on long-term fundamentals. The experiences of the first half serve as a reminder that markets rarely move in straight lines and that successful investing requires patience, discipline, and an appreciation for the complex interplay of factors that drive financial market performance. As we move into the second half of 2025, these lessons will continue to be relevant for investors seeking to navigate an increasingly complex global financial landscape.